This section explains how to request more details about your specific benefits. It describes reciprocal benefits, Qualified Domestic Relations Orders, federal benefit limits and Plan mergers. It also provides general information and legally required language about the Plan.

Important Topics

Appeal of Denied Claims

Appeal of Denied Disability Absence Protection

Assignment of Benefits

Qualified Domestic Relations Orders

Federal Limits on Benefit Amounts

Reciprocal Benefits

Plan Mergers

Other Important Information

Pension Benefit Guaranty Corporation

ERISA Rights Statement

Board of Trustees

Important Names and Addresses

Appeal of Denied Claims

When you submit a claim for benefits (age, disability or survivor) the Administrative Office reviews your Plan record and sends you a decision.

The information that follows explains the procedures the Administrative Office follows for notifying you of the decision and what steps you may take if you disagree. Pay special attention to the deadlines that are discussed, as only appeals submitted within the described time frames may be accepted.

Initial Deadline to Decide Claim

If your application for benefits, or your inquiry related to present or future benefits, is denied, your Administrative Office notifies you of the reasons for the denial. The notice explains how you can appeal this decision.

You are notified of the decision on your claim or inquiry no later than 90 days after the Plan receives it unless an extension, up to an additional 90 days, is required by special circumstances. You are notified if an extension is necessary.

Appealing Decision on Claim

Within 60 days after receiving notification that your application or inquiry is denied, you or your authorized representative may appeal in writing to the Plan’s Benefits Review Committee. Personal appearances are not permitted.

Note: The Plan strongly recommends that you contact the Administrative Office before filing an appeal and ask if there is additional information you can provide to support your claim.

Send your appeal to your Administrative Office. State clearly and specifically why you think the decision on your claim or inquiry is incorrect. To help you prepare your appeal, you or your representative, upon request and free of charge, will be provided with reasonable access to, and copies of, all documents, records and other information relevant to your claim for benefits or inquiry related to present or future benefits (other than documents, records or information that are subject to the attorney-client or other privilege).

Your appeal should include any additional supporting evidence and other materials you want the Benefits Review Committee to consider. The Committee will take into account all materials you provide relating to your claim or inquiry, including materials that were sent after your initial claim or inquiry was denied. Before acting on your appeal, the Committee may require that you send additional information it reasonably believes will help in deciding your case.

Normally, the Committee makes a final decision at its next scheduled quarterly meeting after your appeal is received. However, if your appeal is received within 30 days of a meeting, the decision may not be made until the second meeting after your appeal.

In special circumstances, the Committee may delay its decision until the third meeting after your appeal. You are notified if a delay is necessary. After the Committee makes its decision, you are notified of the results as soon as possible. If your appeal is denied in whole or in part, the notice of the Committee’s decision will be sent to you no later than five days after the decision is made.

Before initiating a legal action to recover any benefit under the Plan, to enforce any right under the Plan or to clarify any right to future benefits under the Plan, you must first comply with the benefit claim procedures described above. Thereafter, you may bring a civil action under Section 502(a) of the Employee Retirement Income Security Act of 1974, as amended, following an adverse determination on appeal.

If you receive a denial from your Administrative Office, contact them to discuss the reasons for the denial before you submit an appeal. Plan representatives can explain the appeal process so that you can determine whether to appeal and what documents you should provide.

If you receive a denial from your Administrative Office, contact them to discuss the reasons for the denial before you submit an appeal. Plan representatives can explain the appeal process so that you can determine whether to appeal and what documents you should provide.

Appeal of Denied Disability Absence Protection

Deadlines and Special Claim and Appeal Rules

Deadline Rules. If you apply for special disability protection under the Plan’s disability absence hours rule or under the special recent coverage for disability rule, and that application is denied, your Administrative Office notifies you of its decision on that application no later than 45 days after receiving the application (unless an extension, of up to 30 more days is necessary due to matters beyond the Plan’s control).

There may be a second extension up to an additional 30 days, if necessary, due to matters beyond the Plan’s control. You are notified if an extension is necessary.

The notice of extension describes the additional information, if any, that the Plan needs to review in order to make a determination on your claim for special disability protection. You have 45 days to provide the additional information (or any longer period specified in the Plan’s notice).

When you are asked to provide additional information, your Administrative Office notifies you of the decision within 30 days from the earlier of:

- The date your Administrative Office receives the additional specified information, or

- The end of the 45-day period (or any longer period specified in the Plan’s notice sent to you to provide the additional specified information).

Special Claim Appeal Rules. If you apply for special disability protection, and that application is denied, you have 180 days, rather than 60 days, to file your written appeal of that denial.

If a particular internal rule, guideline, protocol or other similar criterion was relied upon in making the adverse determination on your application for special disability protection, the notice of denial will identify the rule, guideline, protocol or similar criterion. A copy of the internal rule, guideline, protocol or other criterion will be provided to you upon request, free of charge.

If your denied claim for special disability protection was based in whole or in part on a medical judgment, the Benefits Review Committee will consult with an appropriate independent health care professional in deciding your appeal of that denial. The health care professional will not be the individual who was consulted by the Plan about the initial decision on your claim, nor a subordinate of that individual.

If your claim for special disability protection is denied, you will be provided with a discussion of the Plan’s decision, which will include reasons for disagreeing with or not following:

- Views timely provided by you to the Plan of health care of vocational professionals who evaluated you;

- A disability determination regarding you that was made by the Social Security Administration and timely provided by you to the Plan; and

- Views of health care or vocational professionals whose advice was obtained on behalf of the Plan in connection with your claim.

If the Benefits Review Committee denies your appeal for special disability protection, the Plan will provide you, upon request, with the name of the health care professional whose advice was obtained in connection with the appeal.

Before the Benefits Review Committee denies your appeal for special disability protection, the Plan will automatically provide you, free of charge with:

- New or additional evidence considered, relied upon, or generated by the Plan in connection with your claim;

- New or additional rationale(s) relied upon by the Plan in connection with your claim; and

- A reasonable opportunity to respond to this new information.

Assignment of Benefits

For the protection of you and your family, Plan benefits cannot be assigned and are not subject to garnishment or attachment, except as authorized by law. This means that in most cases your pension check cannot be sent by the Plan to a creditor on your behalf. These protections may not protect your pension benefits from federal tax levies. They also do not apply to Qualified Domestic Relations Orders (QDROs).

Qualified Domestic Relations Orders

A state court can only order the Pension Trust to pay a portion of your benefits to your spouse, former spouse or a dependent as alimony, spousal or child support or in satisfaction of marital property rights if the order is a Qualified Domestic Relations Order (QDRO).

Several key requirements must be met for an order to be considered a QDRO:

- An order must clearly identify the plan participant, alternate payee and name of the Plan to which the order applies. This includes the last known mailing address for the participant and alternate payee.

- An order must clearly state how much of the participant’s benefit is to be paid to the alternate payee and when payments are to begin.

- An order must clearly state what happens when the participant and/or alternate payee dies.

Once the order is entered by the court, a signed, official copy must be provided to your Administrative Office so the Pension Trust can make a formal determination whether the order meets all applicable requirements to be considered a QDRO. The order is not enforceable unless it is determined to be a QDRO.

Before you prepare a proposed QDRO for the court, you or your legal counsel should request a QDRO Information Packet from your Administrative Office. This packet describes the Plan’s requirements for a QDRO and includes Model Provisions for a Qualified Domestic Relations Order and an explanatory memorandum prepared by the Pension Trust’s legal counsel.

You can also obtain without charge a copy of the procedures the Pension Trust follows when determining if a state court order meets the requirements to be considered a QDRO.

If you are currently going through a divorce, you or your legal representative should contact your Administrative Office for specific information regarding your Plan status. Plan representatives can provide information on your Plan coverage and determine the portion of your normal retirement benefit that was earned during your marriage.

Model Provisions

There are two principal types of Model Provisions that the Pension Trust can provide to your legal counsel, depending on whether or not you are retired at the time of your divorce:

- Separate Interest QDRO

- Shared Interest QDRO

Both types of Model Provisions use the time rule to determine the portion of your benefit that is subject to division in your marriage dissolution proceeding. See discussion that follows on the time rule. If you or your attorney want to use a different formula, contact your Administrative Office for assistance.

Separate Interest Model Provisions. The Separate Interest Model Provisions can be used if your QDRO is submitted to the Plan before you retire. This model should be used when an alternate payee wishes to receive pension benefits based on his or her lifetime rather than the participant’s lifetime.

A Separate Interest QDRO is calculated without regard to when the participant’s payments start and without regard to the form of benefit payment the participant elected. Under a Separate Interest QDRO the participant’s benefit is divided into two separate parts—one for the participant and one for the alternate payee.

The alternate payee may begin his or her payments before the participant and receive benefits over his or her lifetime rather than the participant’s lifetime. This means that the alternate payee may begin receiving his or her benefit as early as the participant’s earliest retirement date (see the Early Retirement section), even if the participant has not retired yet. Also, the alternate payee can choose his or her form of benefit payment.

Shared Interest Model Provisions. The Shared Interest Model Provisions must be used if your QDRO is submitted to the Plan after you retire. They can also be used instead of the Separate Interest Model Provisions if you are not yet retired.

With this model, the participant and alternate payee share each benefit payment. The alternate payee cannot start receiving benefits before the participant. Payments under a Shared Interest QDRO stop when the participant dies or stops receiving benefits. Certain death and survivor benefits may also be awarded to an alternate payee after the participant's death.

Time Rule

The time rule is the formula most commonly used by family law judges to determine the portion of your benefit that is community or marital property subject to division in your marriage dissolution proceeding. This formula looks at the amount of time you have been a Plan participant during your marriage as a percentage of the total time you are a participant in the Plan. That percentage is then applied to your total retirement benefit to come up with the portion that is community or marital property. Usually, the non-participant spouse is then awarded one-half of the percentage of your total benefit earned during the marriage, although the parties may agree on a different allocation.

Notifying the Pension Trust of Your Dissolution

Keeping the Pension Trust updated on the status of your divorce and providing copies of your filed final order is extremely important. If your former spouse is awarded an interest in your benefits, it is also important that he or she keeps the Pension Trust advised of any address changes.

If you are the spouse or former spouse of a participant and a QDRO awards you a portion of the participant’s pension, you can begin drawing benefits when the participant reaches earliest retirement age (usually age 55, or earlier if the participant is eligible to retire under a PEER Program or the Rule of 84). You should contact your Administrative Office for specifics about when you can begin receiving benefits.

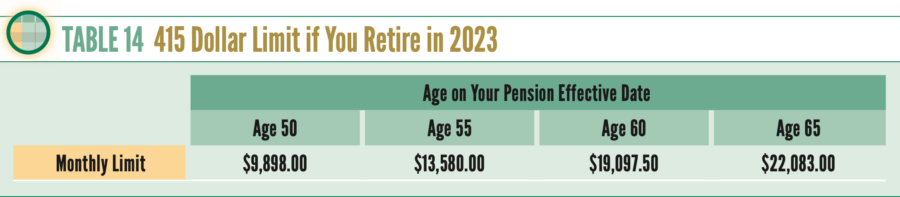

Federal Limit on Benefit Amounts

The federal tax code states that the monthly retirement benefit you receive from the Plan cannot exceed certain dollar maximums (sometimes called the 415 Dollar Limit). The amount of your 415 Dollar Limit depends on your age at retirement and the year when you retire. The younger you are at retirement, the lower the 415 Dollar Limit that applies.

Click here to see the monthly 415 Dollar Limit for participants retiring in 2023 at sample ages.

{kind=link}

If your retirement benefit under regular Plan rules is higher than the 415 Dollar Limit, then the law makes your Plan adjust your benefit amount down so that it does not exceed this limit. This limit can also reduce the amounts your family receives from the Plan after your death.

How the 415 Dollar Limit Works

Let’s say you decide to retire in 2023 at age 55. Assume that your monthly benefit is $5,500 under regular Plan rules.

Here are the steps the Plan must follow to see if the 415 Dollar Limit applies:

Step 1—The Plan determines your 415 Dollar Limit. Since you are retiring in 2023 at age 55, your monthly 415 Dollar Limit from above is $13,580.00.

Step 2—The Plan checks if the $5,500 benefit amount is higher than your 415 Dollar Limit of $13,580.00. Since it is not, the 415 Dollar Limit does not apply.

Dollar Limit Adjustments

If you receive your retirement benefit in some form other than an employee and spouse pension (regular or optional), the law requires that the Plan make certain adjustments when your 415 Dollar Limit is figured.

Contact your Administrative Office if you have questions about how the limit works.

Plan Mergers

Former Western States Food Processing Industry Employees Pension Plan Participants

At the end of December 2001, the Western States Food Processing Industry Food Employees Pension Plan (Western States Food Plan) was merged into the Western Conference of Teamsters Pension Plan. The Western Conference of Teamsters Pension Plan assumed responsibility for administering the Western States Food Plan.

If you were ever covered by the Western States Food Plan, you may be eligible to have your pre-2002 service under the Western States Food Plan recognized as service under the Western Conference of Teamsters Pension Plan. Also, you may be eligible to have your post-2001 service under the Western Conference of Teamsters Pension Plan recognized as Western States Food Plan service to determine your right to receive any benefits you may have earned under that Plan before 2002.

When you apply for retirement, the Western States Food Plan benefits you earned before the merger will be combined with the Western Conference of Teamsters Pension Plan benefits you earned before and after the merger. Similar rules apply if you die before retirement.

Once your pension benefits under each Plan are calculated under that Plan’s rules, then with limited exceptions the Western Conference of Teamsters Pension Plan’s rules will apply to your entire combined benefit to determine such things as:

- Your eligibility for normal, disability or early retirement (including PEER/80, Rule of 84 and recent coverage) and the retirement factors that will be applied to your combined pension benefit, and

- The forms of payment you have for that benefit (click here for more information), and

- The death and survivor benefits payable to your Plan beneficiary upon your death. Click here for more information.

Exceptions. Here are some exceptions to the general rule explained in this section:

Vesting and Loss of Benefits. The Western States Food Plan vesting and loss of benefits rules, modified to reflect the merger, determine your vested status in your Western States Food Plan benefits. These rules will also determine whether you forfeited all or any part of those benefits before retirement.

Special Grandfather Protections. For most participants, the Western Conference of Teamsters Pension Plan rules provide equal or better retirement benefits than the Western States Food Plan would have without the merger.

In those rare instances where a former Western States Food Plan participant would not receive enhanced retirement benefits under the Western Conference of Teamsters Pension Plan rules because of the merger, special grandfather protections are available which the participant can choose upon retirement.

If you are a participant who chooses the special grandfather protections at retirement, your Western States Food Plan benefit and your Western Conference of Teamsters Pension Plan benefit are not combined but kept separate and processed as explained next.

Western States Food Plan Benefit. If you choose the special grandfather protections for your Western States Food Plan benefit at retirement, then Western States Food Plan rules apply to your entire Western States Food Plan benefit. These rules are used to determine such things as:

- Your vested status in that benefit, and

- Your eligibility for normal or early retirement (including PEER/84 and recent coverage) and the retirement factors that apply to your Western States Plan pension benefit, and

- The forms of payment you have for that benefit, and

- The benefits payable to your Plan beneficiary upon your death based on your Western States Food Plan participation. Note that the dependent survivor benefit is eliminated under the Western States Food Plan for participants who die after December 31, 2001.

Important Note: The dependent survivor benefit is eliminated under the Western States Food Plan for participants who die after December 31, 2001. In addition, disability retirement benefits are eliminated under the Western States Food Plan for this purpose if your disability onset date is after December 31, 2001. Note that PEER/80 and the Rule of 84 are not available under the Western States Food Plan as early retirement options.

To the extent necessary, your covered hours under the Western Conference of Teamsters Pension Plan after the merger are considered Western States Food Plan covered hours when applying the Western States Food Plan rules explained above.

Western Conference of Teamsters Pension Plan Benefit. If you choose the special grandfather protections for your Western States Food Plan benefit at retirement, then your Western Conference of Teamsters Pension Plan benefit is limited to the benefit you earned for your covered work under the Plan through December 31, 2001. Your covered work after that date is not counted in determining that benefit.

The Western Conference of Teamsters Pension Plan rules are then applied to determine such matters as:

- Your vested status in that benefit, and

- Your eligibility for normal, disability or early retirement (including PEER, Rule of 84 and recent coverage) and the retirement factors that apply to your limited Western Conference of Teamsters Pension Plan pension benefit, and

- The forms of payment you have for that benefit. (Click here for more information), and

- The death and survivor benefits payable to your Plan beneficiary upon your death based on your Western Conference of Teamsters Pension Plan participation up through 2001. (Click here for more information.)

If you were ever a participant in the Western States Food Plan, when you near retirement, your Administrative Office can help you understand how your benefits are calculated and how to make any decisions regarding benefits affected by the merger.

Former Local 85 Plan Participants

At the end of December 1981, the San Francisco Local 85 Drivers and Helpers Pension Plan (Local 85) merged into the Western Conference of Teamsters Pension Plan. The Western Conference of Teamsters Pension Plan assumed responsibility for administering the Local 85 Plan.

If you were ever covered by the Local 85 Plan, you may be eligible to have your pre-1982 service under the Local 85 Plan recognized as service under the Western Conference of Teamsters Pension Plan. Also, you may be eligible to have your service after 1981 under the Western Conference of Teamsters Pension Plan recognized as Local 85 Plan service to determine your right to receive any benefits you may have earned under the Local 85 Plan before 1982.

Contact your Administrative Office if you were ever a participant in the Local 85 Plan.

Former Southern California Rock Products Teamster Plan Participants

In January 1988, the Southern California Rock Products and Ready Mix Concrete Industries Teamster Employees Retirement Plan (Rock Products Plan) merged into the Western Conference of Teamsters Pension Plan. The Western Conference of Teamsters Pension Plan assumed responsibility for administering the Rock Products Plan.

If you were ever covered by the Rock Products Plan, you may be eligible to have your pre-1988 service under the Rock Products Plan recognized as service under the Western Conference of Teamsters Pension Plan. Also, you may be eligible to have your post- 1987 service under the Western Conference of Teamsters Pension Plan recognized as Rock Products Plan service to determine your right to receive any benefits you may have earned under that plan before 1988.

Contact your Administrative Office if you were ever a participant in the Rock Products Plan.

Former Frozen Foods Employees Pension Plan Participants

In January 1996, the Frozen Foods Employees Pension Plan (Frozen Foods Plan) was merged into the Western Conference of Teamsters Pension Plan. The Western Conference of Teamsters Pension Plan assumed responsibility for administering the Frozen Foods Plan.

If you were ever covered by the Frozen Foods Plan, you may be eligible to have your pre-1996 service under the Frozen Foods Plan recognized as service under the Western Conference of Teamsters Pension Plan. Also, you may be eligible to have your post-1995 service under the Western Conference of Teamsters Pension Plan recognized as Frozen Foods Plan service to determine your right to receive any benefits you may have earned under the Plan before 1996. Contact your Administrative Office if you were ever a participant in the Frozen Foods Plan.

Reciprocal Benefits

The Board of Trustees has entered into the 1997 Teamsters National Reciprocal Agreement and also has individual two-party reciprocal agreements with many other Teamster multiemployer defined benefit pension plans throughout the United States, including the Central States, Southeast and Southwest Areas Pension Plan. Plan rules do not permit reciprocal agreements with single employer pension plans or any kind of defined contribution plan.

If you move from a job covered by this Plan to a job that is covered under another Teamster plan that has a reciprocal agreement with this Plan, you may be eligible for reciprocal benefits from both plans. The same is true if you move to a job covered by this Plan from a job covered by another Teamster plan and there is a reciprocal agreement between both plans.

If you work under another Teamster multiemployer plan outside the 13 Western states, contact your Administrative Office to find out if there is a reciprocal agreement between both plans. If there is no reciprocal agreement, your Administrative Office asks the other Teamster plan if they will sign one so you can qualify for reciprocal benefits under both plans.

Reciprocal eligibility requirements vary between plans. To be considered eligible for reciprocal eligibility under this Plan, you must have completed at least 3,000 covered hours or been an active participant at some point before your pension effective date. Additionally, you must:

- Apply for benefits with each pension plan, and

- Satisfy severance and reemployment requirements under each pension plan, and

- Be determined eligible for a reciprocal benefit under each plan.

Each plan will calculate your benefit based on its own plan rules. Under the Western Conference of Teamsters Pension Plan, your reciprocal benefit will be calculated based on your combined credit with all participating reciprocal plans and compared to the credit you earned solely under the Western Conference of Teamsters Pension Plan. This calculation determines the percentage of your total combined benefit that will be paid by the Western Conference of Teamsters Pension Plan (sometimes referred to as the “percentage of liability”).

Note: Because the research required to determine eligibility for a reciprocal pension can take longer than 90 days, you should contact your Administrative Office at least six months before your actual pension effective date. Otherwise, your benefit payments may be delayed.

Other Important Information

Contributions to the Pension Trust

Contributions to the Pension Trust are made by covered employers based on their collective bargaining agreements with Teamster local unions. Contributions by employees are not required or permitted.

Plan Documents

You can read the governing Plan documents at your Administrative Office during business hours without charge. These documents include the official text of the Pension Plan, the Trust Agreement and the collective bargaining agreement you work under if it provides for employer contributions to the Pension Trust. Other Plan documents include your Plan’s annual financial reports (Form 5500), the Summary Plan Booklet and any updates to this booklet (Summary of Material Modifications).

Most of these documents are available on this website at the Plan Forms and Documents page. You may also request a copy of a governing Plan document by sending a written request to your Administrative Office describing the documents you want. In most cases, there is a charge to cover copying costs. You may be required to pay in advance. You can ask about the charge beforehand. There is no charge to obtain a copy of the current Pension Plan or Trust Agreement.

Annual Funding Notice

The Pension Protection Act of 2006 (PPA) requires that pension plans provide an Annual Funding Notice to participants and beneficiaries within 120 days after the close of the plan year.

The funding notice provides information regarding the Plan’s funded current liability percentage and a comparison of the Plan’s assets to benefit payments.

The funding notice is mailed by April of each year to your current home address. If you do not receive a copy, please contact your Administrative Office.

You may also request in writing copies of certain actuarial and financial information about the Plan. The information you can request consists of the following:

- A copy of any periodic actuarial report (including sensitivity testing) received by the Plan for any plan year which has been in the Plan’s possession for at least 30 days.

- A copy of any quarterly, semiannual or annual financial report prepared for the Plan by any of the Plan’s investment managers, the Plan’s investment advisor or any fiduciary which has been in the Plan’s possession for at least 30 days. These reports include the investment advisor’s quarterly investment report to the Trustees which summarizes performance data contained in the periodic reports from each of the Plan’s investment managers and un-audited quarterly financial statements prepared by the Plan’s Administrative Manager for the Trustees.

- Any application filed with the Secretary of the Treasury requesting an amortization extension under ERISA (if applicable).

The PPA exempts certain information from disclosure such as information that is proprietary to an investment manager.

The documents will be provided to you within 30 days from the date your request is received by the Pension Trust. A service fee will be charged for copying costs and mailing.

Collective Bargaining Agreements

Your Plan is maintained under collective bargaining agreements between nearly 100 local unions affiliated with the International Brotherhood of Teamsters and more than 1,460 covered employers.

You can get a copy of your collective bargaining agreement from your local union or employer. You can also read these agreements free of charge at your Administrative Office or request a copy for a charge.

Covered Employers and Unions

You may review free of charge a complete list of covered employers and local unions sponsoring the Plan (along with their addresses) by visiting your Administrative Office during business hours. You may also request a copy by writing to your Administrative Office.

Upon written request to your Administrative Office, you can find out if a particular employer is a covered employer, or if a particular local union represents employees covered by the Plan, and if so that employer’s or union’s address.

Requests for Plan Materials

If you make a written request to an Administrative Office for material that your Plan is required to give you, you should receive the material within 30 days. However, due to matters beyond your Plan’s control (for example, your request is lost in the mail), the material may reach you more than 30 days after your request.

Please contact your Administrative Office if you don’t receive the requested material within 30 days and they will send you another copy immediately.

Source of Benefits

Your pension benefits are paid to you from the assets of the Pension Trust.

Plan Identification Numbers. The Plan may be referred to by the Employer Identification Number 91-6145047, and Plan Identification Number 001.

Your Plan's Fiscal Year. Your Plan’s fiscal year is the calendar year January 1 through December 31.

Type of Plan

Your Plan is a multiemployer defined benefit pension plan. This means that many different employers contribute to the Pension Trust on behalf of their employees. It also means that your benefits are based on a set formula so that your future benefit can be determined by this formula. Retirement benefits in general are paid as monthly benefits over a participant’s lifetime.

Board of Trustees

Your Plan is administered by a Board of Trustees. Half of the Trustees are representatives chosen from the unions and the other half are representatives chosen from covered employers or employer associations. The Board of Trustees makes the decisions regarding any question, interpretation and application of Plan provisions and is responsible for seeing that Plan provisions are applied in a uniform manner.

The Board of Trustees has chosen independent contract administrators as the Administrative Offices to take care of Plan operations. The addresses and phone numbers for these offices are listed on the Contact page.

Plan Investments

The Board of Trustees holds all assets of the Plan in the Pension Trust for the sole benefit of Plan participants and beneficiaries. These assets are managed by professional investment managers following strict policies monitored by the Board of Trustees.

Plan Amendment or Termination

The Board of Trustees has the power to amend or terminate the Plan at any time.

Plan Amendment. Plan amendments may modify benefit levels and change eligibility requirements. Subject to legal restrictions, these Plan amendments may apply to you even if they result in lower benefit levels and stricter eligibility rules.

Except as required by law, Plan amendments cannot adversely affect any benefits that are already being paid to a pensioner, surviving spouse or surviving children.

In certain circumstances, federal law might require changes in the Plan resulting in reduced benefits. This could happen, for example, if your Plan faces severe financial difficulties.

Plan Termination. Should the Plan terminate, the assets of the Pension Trust can never be used for any other purpose than to provide Plan benefits and pay reasonable administrative expenses of the Pension Trust.

If there are not enough assets in the Pension Trust when the Plan terminates to pay all the benefits each person is entitled to receive, the law establishes priorities on how benefits are paid. This could mean that an individual would receive a smaller pension than if the Plan had continued. Some individuals who are not vested may receive no benefits at all. However, as explained next, the Pension Benefit Guaranty Corporation, by law, guarantees that certain vested benefits are paid in the event of Plan termination even if the Plan does not have sufficient assets.

Pension Benefit Guaranty Corporation

Your pension benefits under this multiemployer plan are insured by the Pension Benefit Guaranty Corporation (PBGC), a federal insurance agency. A multiemployer plan is a collectively bargained pension arrangement involving two or more unrelated employers, usually in a common industry.

Under the multiemployer plan program, the PBGC provides financial assistance through loans to plans that are insolvent. A multiemployer plan is considered insolvent if the plan is unable to pay benefits (at least equal to the PBGC’s guaranteed benefit limit) when due.

The maximum benefit that the PBGC guarantees is set by law. Under the multiemployer plan program, the PBGC guarantee equals a participant’s years of benefit service multiplied by:

- 100% of the first $11 of the monthly benefit accrual rate, plus

- 75% of the next $33 of the monthly benefit accrual rate.

The PBGC does not have a dollar limit on the monthly benefit payable under a multiemployer plan only a limit on the benefit rate used to calculate the monthly benefit.

The PBGC guarantee generally covers:

- Normal and early retirement benefits, and

- Disability benefits if you become disabled before the plan becomes insolvent, and

- Certain benefits for your survivors.

The PBGC guarantee generally does not cover:

- Benefits greater than the maximum guaranteed amount set by law, and

- Benefit increases and new benefits based on Plan provisions that have been in place for fewer than five years at the earlier of:

-

- The date the Plan terminates or

- The time the Plan becomes insolvent, and

- Benefits that are not vested because you have not worked long enough, and

- Benefits for which you have not met all of the requirements at the time the Plan terminates, and

- Non-pension benefits, such as health insurance, life insurance, certain death benefits, vacation pay and severance pay.

For more information about the PBGC and the benefits it guarantees, ask your Administrative Office or contact:

PBGC

P.O. Box 151750

Alexandria, VA 22315-1750

You can also call the PBGC at (800) 400-7242 or (202) 326-4000. TTY/TDD users may call the federal relay service toll-free at (800) 877-8339 and ask to be connected to (202) 400-7242.

Additional information about the PBGC’s pension insurance program is available through the PBGC’s web site at www.pbgc.gov.

ERISA Rights Statement

The statement below is a summary—written by the U.S. Department of Labor—of your rights as a Plan participant that ERISA guarantees.

As a participant in the Western Conference of Teamsters Pension Plan you are entitled to certain rights and protections under the Employee Retirement Income Security Act of 1974 (ERISA). ERISA provides that all Plan participants shall be entitled to:

Receive Information about your Plan and Benefits

Plan Documents. Examine, without charge, at any of the Plan’s Administrative Offices, and at other specified locations, such as work sites and union halls, all documents governing the Plan, including insurance contracts and collective bargaining agreements, and a copy of the latest annual report (Form 5500 Series) filed by the Plan with the U.S. Department of Labor and available at the Public Disclosure Room of the Employee Benefits Security Administration.

Obtain, upon written request to any of the Plan’s Administrative Offices, copies of documents governing the operation of the Plan, including insurance contracts and collective bargaining agreements, and copies of the latest annual report (Form 5500 Series) and updated summary plan description. The Pension Trust may make a reasonable charge for the copies.

Annual Funding Notice. Receive basic information about the funding status and the financial condition of the Plan including the Plan’s funding percentage, assets and benefits guaranteed by the PBGC.

Statement of Accrued and Vested Pension Benefits. Obtain a statement telling you whether you have a right to receive a pension at normal retirement age (usually age 65) and if so, what your benefits would be at normal retirement age if you stop working under the Plan now. If you do not have a right to a pension, the statement will tell you how many more years you have to work to get a right to a pension. This statement must be requested in writing from your Administrative Office and is not required to be given more than once every 12 months. The Plan must provide the statement free of charge.

Prudent Actions by Plan Fiduciaries

In addition to creating rights for plan participants, ERISA imposes duties upon the people who are responsible for the operation of the employee benefit plan. The people who operate your plan, called “fiduciaries” of the plan, have a duty to do so prudently and in the interest of you and other plan participants and beneficiaries. No one, including your employer, your union, or any other person, may fire you or otherwise discriminate against you in any way to prevent you from obtaining a pension benefit or exercising your rights under ERISA.

Enforcing Your Rights

If your claim for a pension benefit is denied or ignored in whole or in part, you have a right to know why this was done, to obtain copies of documents relating to the decisions without charge, and to appeal any denial, all within certain time schedules.

Under ERISA, there are steps you can take to enforce the above rights. For instance, if you request a copy of plan documents or the latest annual report from the plan and do not receive them within 30 days, you may file suit in a federal court. In such a case, the court may require the plan administrator to provide the materials and pay you up to $110 a day until you receive the materials, unless the materials were not sent because of reasons beyond the control of the administrator.

If you have a claim for benefits which is denied or ignored, in whole or in part, you may file suit in a state or federal court. If it should happen that plan fiduciaries misuse the plan’s money, or if you are discriminated against for asserting your rights, you may seek assistance from the U.S. Department of Labor, or you may file suit in a federal court. In addition, if you disagree with the plan’s decision or lack thereof concerning the qualified status of a domestic relations order, you may file suit in a federal court. If it should happen that plan fiduciaries misuse the plan’s money, or if you are discriminated against for asserting your rights, you may seek assistance from the U.S. Department of Labor, or you may file suit in a federal court. The court will decide who should pay court costs and legal fees. If you are successful the court may order the person you have sued to pay these costs and fees. If you lose, the court may order you to pay these costs and fees, for example, if it finds your claim is frivolous.

Assistance with Your Questions

If you have any questions about your plan, you should contact the plan administrator. If you have any questions about this statement or about your rights under ERISA, or if you need assistance in obtaining documents from the plan administrator, you should contact the nearest office of the Employee Benefits Security Administration, U.S. Department of Labor, listed in your telephone directory or the Division of Technical Assistance and Inquiries, Employee Benefits Security Administration, U.S. Department of Labor, 200 Constitution Avenue N.W., Washington, D.C. 20210. You may also obtain certain publications about your rights and responsibilities under ERISA by calling the toll-free hotline of the Employee Benefits Security Administration at (866) 444-3272.

Click here for questions and answers about Other Information.

Board of Trustees

Union Trustees

Chuck Mack

Union Chairman

Mark Davison

Tony Delorio

Peter Finn

Lourdes Garcia

Rick Hicks

Spencer Hogue

Samantha Kantak

Felix Martinez

Victor Mineros

Chris R. Muhs

Karla Schumann

Jaime Vasquez

Employer Trustees

Rick E. Porter

Employer Chairman

Brent R. Bohn

Patrick J. Callans

Jeff A. Carlsen

Scott Guensler

James R. Ham

Joseph F. Hodge

Robert L. Hutchison

Chris Langan

Lindsay Marshall

John A. Ontiveros

Andrew Sweet

Darin J. Torosian

Plan Administrator

Board of Trustees

Western Conference of Teamsters Pension Plan

2323 Eastlake Avenue East

Seattle, WA 98102-3393

(206) 329-4900 or (800) 531-1489

Administrative Offices

Northwest/Rocky Mountain Administrative Office

Western Conference of Teamsters Pension Plan

2323 Eastlake Avenue East

Seattle, WA 98102-3393

(206) 329-4900 or toll-free (800) 531-1489

Northern California Administrative Office

Western Conference of Teamsters Pension Plan

1000 Marina Boulevard, Suite 400

Brisbane, CA 94005-1841

(650) 570-7300 or toll-free (800) 531-1489

Southwest Administrative Office

Western Conference of Teamsters Pension Plan

225 South Lake Avenue, Suite 1200

Pasadena, CA 91101-3000

(626) 463-6100 or toll-free (800) 531-1489

Regional Service Center

Western Conference of Teamsters Pension Plan

700 NE Multnomah Street, Suite 350

Portland, OR 97232-4197

(503) 238-6961 or (800) 531-1489

Pension Plan Agent for Service of Legal Process

Michael M. Sander

Administrative Manager

Western Conference of Teamsters Pension Plan

2323 Eastlake Avenue East

Seattle, WA 98102-3393

(206) 329-4900 or toll-free (800) 531-1489

Your Plan Website

Check out your Plan’s website at www.wctpension.org